The Impact of Your Credit Score on Home Loan Eligibility

shubham

Buying a home is an exciting journey, but it also involves careful financial planning. One key factor that influences your ability to secure a home loan is your credit score. Understanding how your credit score affects your mortgage eligibility can help you prepare better and make informed decisions. Here’s a simple guide to help you understand how your credit score affects your home loan eligibility and what you can do to improve it.

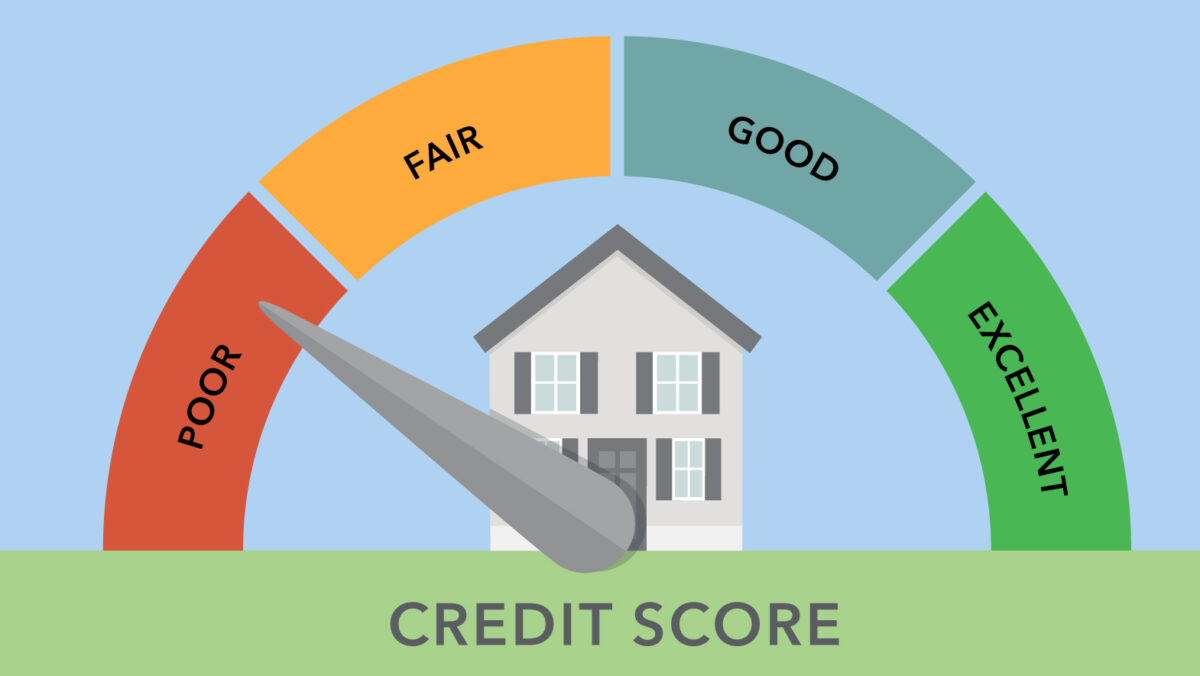

A credit score is a three-digit number that reflects your creditworthiness, or how likely you are to repay borrowed money. Your credit score is calculated using data from your credit report based on your credit history, including your borrowing and repayment patterns. Credit scores typically range from 300 to 850, with higher scores indicating better credit health.

To improve your credit score before applying for a home loan, pay bills on time, reduce credit card balances, check your credit reports for errors, and avoid new credit applications.

Here are some effective steps you can take:

Check Your Credit Report: Obtain and review your credit report from major credit bureaus. Look for errors or inaccuracies and dispute any mistakes you find.

Related Post: What is a Loan Against Property?

A mortgage professional can provide personalized advice based on your financial situation. They can help you understand how your credit score impacts your loan options and guide you through the application process.

Your credit score is an essential factor in securing a home loan and can influence both your approval chances and the terms of your mortgage. By understanding its impact and taking proactive steps to improve your credit health, you can enhance your chances of obtaining favorable loan conditions and achieving your dream of homeownership. Remember, good credit management is a long-term commitment, but the benefits are well worth the effort.

If you’re unsure about your credit score or need personalized advice, consider consulting with a financial advisor – Shubham Housing Finance. They can provide easy guidance and help you navigate the home loan process with greater confidence.

All Rights Reserved © 2023